According to RocketMortgage, the average mortgage term is 30 years and the average length is under 10 years. This is because homeowners will either refinance their home, like I did to get a much lower interest rate, or because they want to move. Refinancing your mortgage to get a lower interest rate makes sense if the new rate will be much lower such that you’ll end up saving money. You’ll just have to keep in mind that if you’ve had your mortgage for 10 years, for example, and you refinance, the clock resets and you’ll have 30 years to pay off your mortgage instead of 20. For this reason, I personally continue to pay the same monthly payments at the higher interest rate so that I pay less interest and the mortgage is paid off sooner.

But what if you sell your home to buy a new one within 10 years? What many people may not realize is that by doing this, they will lose a lot of money because their home loan is an amortized loan rather than a simple interest loan. Amortized loans favor lenders, like banks, instead of borrowers. Unlike a simple interest loan, where you’re paying the same amount towards principal and interest each month, when you get a mortgage, most of your monthly payments go towards interest in the beginning and less near the end of the 30-year term.

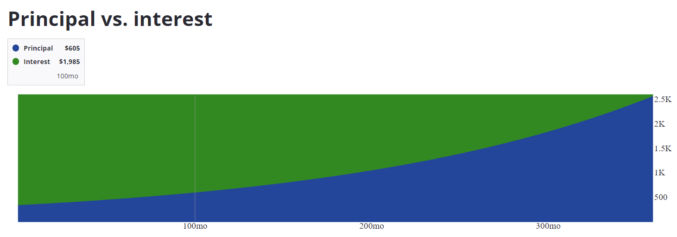

Note that your total interest payments over 30 years is more than the loan amount.

Let’s take a few points in time and compare how much of your monthly payment goes towards principal and interest.

Principal

Interest

Percent Towards Interest

First mortgage payment

$346

$2244

86.64%

Mortgage payment at month 100 (8.3 years)

$605

$1985

76.64%

Mortgage payment at month 200 (16.7 years)

$1058

$1531

59.13%

Mortgage payment at month 236 (19.7 years)

$1294

$1295

50%

Mortgage payment at month 300 (25 years)

$1851

$738

28.51%

Mortgage payment at month 360 (30 years)

$2578

$14

0.54%

As you can see, in the first 10 years of your mortgage, the bulk of your monthly payments goes towards paying interest. Your equity from paying down the principal is very little. Therefore, if you sell your house within the first 10 years and buy a new one, you’ll have little equity from your mortgage payments and, when you get a new mortgage for your new home, you’ll start over from month 1, when most of your new monthly payments will go towards interest again.

Of course, your house could appreciate significantly in 10 years, in which case the equity you gain from appreciation could outweigh the equity from paying off the principal. However, that is not always the case.

If you’re planning on selling your home within 10 years and buying a new one, it may not be worth it since you may lose a lot of money from having mostly just paid interest.

I just finished renovating one of my rental apartments. I took a bunch of photos and, though the apartment looks nice, it looks extremely plain and uninviting without furniture. Some people have a good imagination and sense of design and can visualize what a room could look like with furniture the right furniture, but most people are clueless when it comes to interior design. I definitely don’t want to spend a lot of time, money, and energy paying a professional stager to come and bring real furniture to my apartment. Fortunately, there are online services where you can pay companies (or individuals) to virtually stage photos of your rooms for you. Or, you can use one of many DIY websites where you can virtually stage your rooms yourself.

After doing some research, I came across Apply Design. They charge up to $10 per photo. You can try it for free on one photo. So, I gave it a try and here’s what I came up with.

Living Room When Occupied by Tenant

The photo is distorted because I used a 360-degree camera placed in the center of the room. To show more of the room, I had to zoom out which made the walls look wider or narrower.

Living Room Right After I Kicked Out My Inherited Tenant

Again, the photo above is distorted.

Living Room After Renovating It

The photo above is the one I uploaded to Apply Design.

Virtually Staged Photo (Before Rendering)

This is how the living room looked after I drag and dropped furniture and design elements onto the previous photo but before rending the objects.

Virtually Staged Photo (After Rendering)

This is the final, rendered version of the photos. As you can see, it not only looks realistic, but it looks way more attractive and inviting than the empty room. When you compare it to the pre-rendered version, you see much more detail, shadows and vibrant colors.

How it Works

Virtually staging a room is actually very easy. Here are the steps using Apply Design.

Upload photos Apply Design will take a few minutes to analyze each photo. I think it’s trying to determine where the walls are and the depth of field.

Drag furniture and interior elements You can search or browse for furniture and then drag them to your photo. You can edit each object by moving, resizing, rotating, etc.

Render a photo Rendering a photo takes around 5-10 minutes.

Overall, I think this is a great way to improve your home sale or rental potential.

Other Examples

Bedroom when occupied by tenantsBedroom after (necessarily) renovating itBedroom after virtually staging itMaster bedroom when occupied by tenantsMaster bedroom after (necessarily) renovating itMaster bedroom after virtually staging itBeforeAfter virtual staging

I’ve used many enterprise-level productivity tools like Atlassian Jira, Confluence (Wiki), Microsoft Teams, Asana, and, of course, email. Asana seems to be the best for managing large projects that have multiple tasks and deadlines. Microsoft Teams is great for having discussions separated by topic and sharing documents related to each discussion. As the president of an HOA (Homeowner’s Association) that pays an experienced property manager, it’s interesting that we’re still communicating by email because so often we’d have a hard time finding specific information and documents. Microsoft Teams would be a big improvement but the free version doesn’t come with some useful features available in the paid version. Of all the tools I’ve used, it looks like Slack fits the bill because 1) there is no bill (pun intended – there’s a free version) and 2) it comes with features similar to the ones in the paid version of Microsoft Teams. This post will explain some of Slack’s features that could be beneficial for small groups like an HOA.

Separate Discussions By Topic

One of the problems with a simple chat tool is different topics get lost in one super long chat. At my HOA, we have different topics to talk about, e.g. landscaping, security cameras, parking, etc. With Slack, you can create multiple channels to represent these topics. Each channel is a separate chat discussion as you can see in the screenshot below.

In the screenshot above, you can see:

Group Name: Antoine Ct Landlords

Channels: These are discussion topics:

landscaping-cleaning

security-cameras

vehicles-and-parking

Direct messages: this shows you who is in the group and allows you to send a message directly to one specific person

Apps: you can see the list of apps you’ve integrated with Slack such as a polling app

In the screenshot above, the chat in view is the one for the landscaping-cleaning channel.

Apps

Slack allows you to integrate many apps for a seamless experience. Below are some of the apps you can integrate.

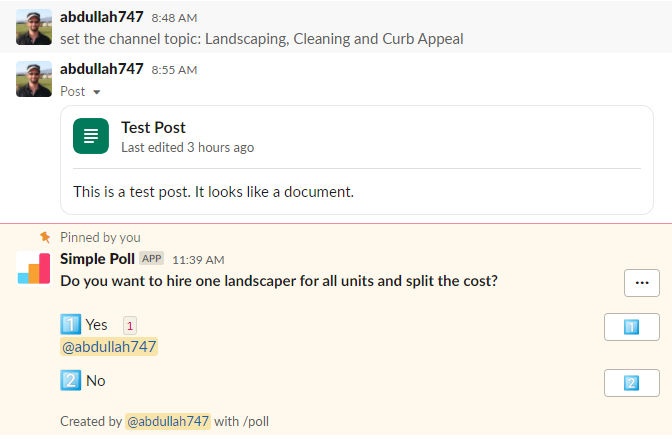

One thing we often do as an HOA is conduct polls. You can add a polling app and then create a poll in a channel. For example, I added the Simple Poll app and created a poll in the landscaping-cleaning channel. In the screenshot below, the simple poll asks if everyone wants to hire one landscaper for all units and split the cost. The answer options are simply yes and no.

Of course, if there is too much chatter, the poll can get buried in the history of chat messages. If that happens, you can pin the poll to the top. It then shows up in the bar at the top of the channel like this:

Links to Documents

Chatting is useful, but eventually you’re going to need other productivity tools like documents, spreadsheets, presentations, etc. In the chat field, you can click the + button to insert things other than text, e.g. create a post.

A post in Slack is like a Google or Word doc.

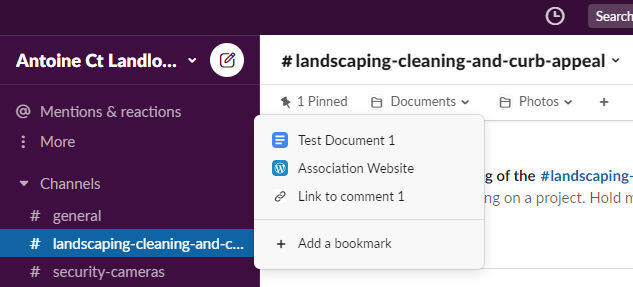

If you prefer to use a different tool like Google Docs, you can link the Google Doc to your Slack channel. Just copy the Google Doc share URL and paste it into the chat and, optionally, pin it to the top as I did for the poll example above. Or, you can create folders in the bar at the top of the channel to organize documents and chat messages. In the screenshot below, I clicked the + button to add two folders: Documents and Photos.

I then hovered over the Documents folder link and clicked Add to bookmark to add links to external resources:

Test Document 1 (link to a shared Google Doc)

Association Website (link to a WordPress site)

Multiple Teams

If you are part of multiple groups or teams of people, you can create a separate Slack group (called Workspaces). In the screenshot below of the Slack homepage, I see the workspace for the example HOA group mentioned above called “Antoine Ct Landlords”. There is also a button to create a new workspace.

If you are part of a small (or large) group of people and need to discuss many topics and don’t want to pay a monthly fee, you may want to give Slack a try.

If you are a real estate investor and have one or more rentals you’ve accumulated over time, there’s a good chance you have a good amount of equity in at least one of your properties – maybe even your primary residence. You might feel happy that you have a lot of equity but from an investment point of view, you could be making more money — potentially A LOT more — if you pull out some of that equity to re-invest it rather than leave it in the form of equity for an existing property. Compare the following two scenarios.

Scenario 1

Let’s say you have 3 properties. One is your primary residence which you live in and are not renting out. The other two are rentals.

Current Value

Equity

Rental Income (monthly)

Primary Residence

$1,000,000

$600,000

$0

Rental 1 (townhouse)

$750,000

$650,000

$2,500

Rental 2 (triplex)

$590,000

$100,000

$4,820

Appreciation

Now, let’s estimate the value + appreciation on each property per year over 10 years. The average annual appreciation rate in California is 6.77%. We can easily calculate the appreciation using the calculator at

In the last row, we see the total appreciation over 10 years.

Year

Primary Residence

Rental 1

Rental 2

1

$1,067,700

$800,775

$629,943

2

$1,139,983

$854,987

$672,590

3

$1,217,160

$912,870

$718,124

4

$1,299,562

$974,671

$766,742

5

$1,387,542

$1,040,657

$818,650

6

$1,481,479

$1,111,109

$874,073

7

$1,581,775

$1,186,331

$933,247

8

$1,688,861

$1,266,646

$996,428

9

$1,803,197

$1,352,398

$1,063,886

10

$1,925,273

$1,443,955

$1,135,911

Diff

$925,273

$693,955

$545,911

Rental Income

Now, let’s estimate the annual gross rental income and per year over 10 years. For simplicity, and to be conservative, we’ll keep the monthly rent fixed (we’ll never increase the rent), although in reality, in California you can legally increase the rent by at least 5% per year. In the last row, we see the total gross rental income over 10 years. Of course, you’ll have expenses like debt service (paying your mortgage), taxes, operational costs, etc which will reduce this total rental income.

Year

Primary Residence

Rental 1

Rental 2

1

0

0

$0

2

0

$30,000

$57,840

3

0

$30,000

$57,840

4

0

$30,000

$57,840

5

0

$30,000

$57,840

6

0

$30,000

$57,840

7

0

$30,000

$57,840

8

0

$30,000

$57,840

9

0

$30,000

$57,840

10

0

$30,000

$57,840

Total

0

$270,000

$520,560

Total Return on Investment

Now, if we add the appreciation and rental income minus expenses over 10 years, we’d get our total return on investment (ROI). But, since expenses vary from one property to another, to be conservative and keep things simple, we’ll just look at the total appreciation.

Over 10 years, our investments will have appreciated by $2,165,140.

Now, let’s compare this to another scenario where we do cash-out refinance and reinvest the money in more rental properties.

Scenario 2

In this scenario, we decide whether to do cash-out refinance for each existing property.

Primary residence

For the primary residence, we won’t refinance it and take cash out because doing so would increase the mortgage and since it’s not a rental, you’d have to pay for that increase yourself. Of course, if you can afford it, you could also do a cash-out refinance on that property as well, but it’s not a good idea to spread yourself too thin.

Rental #1

For rental #1, we do a cash-out refinance to pull out 75% of the equity. In doing so, our monthly mortgage pay for that property will go up but if you plan it correctly, your income will cover your new expenses, especially if your previous loan would be paid off in, say, 10 years, and you refinance to 30 years which would lower your monthly payments despite having borrowed more money.

Rental #2

For rental #2, there isn’t enough equity in the property so we can’t refinance it.

Current Value

Current Equity

Cash-out refi 75% of value

New Equity

Primary Residence

$1,000,000

$600,000

No refi

$600,000

Rental 1

$750,000

$650,000

$562,500

$100,000

Rental 2

$590,000

$100,000

No refi

$100,000

Total

$562,500

According to the table above, we’re able to pull out $562,500 from Rental #1 which we’ll use as a down payment to purchase more rental properties. Let’s say we buy 4 duplexes at $500,000 each and we put down 25% (standard for investment properties) which is $125,000 for each. That leaves us with $62,500 for closing costs and some home improvement. We’ll estimate the rental income for each duplex is $3500 per month.

Current Value

Equity

Rental Income (monthly)

Rental 3 (duplex)

$500,000

$125,000

$3,500

Rental 4 (duplex)

$500,000

$125,000

$3,500

Rental 5 (duplex)

$500,000

$125,000

$3,500

Rental 6 (duplex)

$500,000

$125,000

$3,500

Appreciation

Now, like in scenario 1, let’s estimate the appreciation over 10 years.

Year

Rental 3

Rental 4

Rental 5

Rental 6

1

$533,850

$533,850

$533,850

$533,850

2

$569,992

$569,992

$569,992

$569,992

3

$608,580

$608,580

$608,580

$608,580

4

$649,781

$649,781

$649,781

$649,781

5

$693,771

$693,771

$693,771

$693,771

6

$740,739

$740,739

$740,739

$740,739

7

$790,887

$790,887

$790,887

$790,887

8

$844,431

$844,431

$844,431

$844,431

9

$901,599

$901,599

$901,599

$901,599

10

$962,637

$962,637

$962,637

$962,637

Diff

$428,787

$428,787

$428,787

$428,787

Rental Income

Now, like in scenario 1, let’s estimate the annual gross rental income and per year over 10 years.

Year

Rental 3

Rental 4

Rental 5

Rental 6

1

$42,000

$42,000

$42,000

$42,000

2

$42,000

$42,000

$42,000

$42,000

3

$42,000

$42,000

$42,000

$42,000

4

$42,000

$42,000

$42,000

$42,000

5

$42,000

$42,000

$42,000

$42,000

6

$42,000

$42,000

$42,000

$42,000

7

$42,000

$42,000

$42,000

$42,000

8

$42,000

$42,000

$42,000

$42,000

9

$42,000

$42,000

$42,000

$42,000

10

$42,000

$42,000

$42,000

$42,000

Total

$420,000

$420,000

$420,000

$420,000

Total Return on Investment

Now, let’s calculate the total ROI. Again, to be conservative and for simplicity, we’ll just consider total appreciation even though we know the total ROI will be much more than that since every month for 10 years we’ll be paying down the mortgage using the rental income which increases our equity in each property.

The total appreciation over 10 years in scenarios 1 and 2 are

Therefore, using a very conservative estimate, we could make an additional $1,715,147 over 10 years if we refinanced and reinvested the equity in our existing properties.

What to do after 10 years

Let’s say you hold on to the properties for 10 years. You’ll most likely have a mortgage on all or some of properties. At that point, you could choose to sell some of the properties to pay off all of your mortgages and live mortgage free! You’ll still be getting rental income from the remaining rental properties which may even amount to as much or more as your work income from a day job in which case you could choose to just retire and travel the world.

Following are some ways once can finance the purchase of real estate.

Conventional loan (mortgage)

Most people who buy real estate get a conventional loan and pay a mortgage for 30 years. They typically put a 20% down payment. Most banks, however, don’t want anything to do with a high-risk property that needs work. So to qualify for a conventional loan from a bank, a buyer / investor will first need to get the property up to a living standard.

Private lender

Private lenders are simply individuals, not businesses, who are willing to loan you money, e.g. family and friends. Sometimes, parents may gift their kids the down payment required to purchase a property but behind the scenes, make an agreement so that the kids pay back the money over a period of time. This is necessary since banks / lenders most likely would not allow the borrower to have multiple loans. Borrowing money in this way is easy because it doesn’t involve credit checks, appraisals, underwriting, etc.

Hard money lender

Hard money lenders are companies or funds that will loan you the money for a fee (interest). This process requires credit checks and includes underwriters who also determine the property’s value. Hard money lenders charge higher interest rates and the loans are for a much shorter period of time. The average is 6 months. Unlike private lenders, who often just trust that you’re making a good investment, hard money lenders will double check that your investment is reasonably sound since otherwise, they could lose money if you default.

House hack

House hacking is buying a property and renting a portion of it out to cover your expenses. You could be a 3 bedroom house and rent out 2 of the bedrooms. Or, you could buy a multifamily property (duplex, triplex, etc), and rent out the other units. In doing this, you significantly reduce your monthly expenses because you’ll have tenants paying for a big portion of your mortgage / loan.

Home equity loan

If you already own a home and have equity in it, then you could borrow money against it.

You borrow money against equity in your existing home

The interest rate is typically fixed

If you still have a mortgage, a home equity loan would be a second mortgage behind your first mortgage

You get the entire amount of the loan at once upon closing

HELOC

HELOC stands for Home Equity Line of Credit. If you already own a home and have equity in it, then you could borrow money against it.

You borrow money against equity in your existing home

The interest rate is variable and tied to prime

If you still have a mortgage, a home equity loan would be a second mortgage behind your first mortgage

You get to draw money from the line of credit multiple times (like a credit card)

Refinance

If you have a mortgage on your home, you can refinance the loan to replace it with another one. You typically do this if interest rates have dropped thereby lowering your monthly mortgage payments.

Cash-out refinance

This is like a regular refinance except you also get cash from the equity in your home. You could then use that cash to pay for purchasing another property, for example. The maximum cash you can get is 80% of the value of the home.

Flip

To flip real estate means to buy a fixer upper, renovate it, then turn around and sell it for a profit. houses. Can be mobile homes, single family, multifamily, etc.

Add Square Footage

Residential real estate (including multi-family properties with 4 or less units) is often valued by square footage. One strategy to increase the value of a property is by enlarging it, e.g. by adding bedrooms. If you know how to do this cost effectively, e.g. if you know how to do some or all of it yourself, you can add value and sell the property for a profit. Of course, this will depend a lot on where you live. For example, if you live in the Bay Area where the cost per square foot is very high, adding an addition to an existing property could be worth it.

BRRR method

BRRRR stands for “buy, rehab, rent, refinance, repeat.” With this real estate investment lifecycle, you could

buy a property (whether using a conventional loan from a bank, HELOC, private loan or a hard money loan)

rehab the property to increase it’s value (like fixing up a fixer upper)

rent out the property. Banks rarely want to refinance a property that isn’t occupied, so renting your house comes first.

refinance the property. This is actually a cash-out refinance using a conventional loan from a bank and get cash back. In this step, you would expect the property to appraise for much more than your purchase price because you rehabbed the place. The bank would require an appraisal. Once the appraisal is done, you could get 20% of the appraised value in cash and finance the remaining 80%. You may want to get pre-approved for the AVR before buying the property to ensure you will be able to refinance the property when the time comes.

Waiting for seasoning Many conventional and portfolio lenders require properties to “season” first. Seasoning means you’ll need to wait between six and 12 months before refinancing. If you’re using a private or hard money lender, it’s imperative to calculate exactly how much this period of time will cost you.

repeat. Using the cash you got from step 4, you would use it towards buying another property so you could repeat the entire process all over again

The key to the success of the BRRRR method is to

buy properties under market value

never investing more than 75% of the property’s after-repair value (ARV)

ensure that you can rent the property at a rate that will cover your expenses by looking a rental comps

Let’s say that you find a property that is in disrepair. It’s been on the market for a while because no one wants to fix it up. You determine that the repairs are mostly or all cosmetic and not structural (e.g. foundation, etc). You estimate the value of the property after you repair it to be $500K based on nearby comparables, Zillow Zestimates, etc. You also estimate it would cost you $60K to fix it up. Therefore, based on the following equation

purchase price + rehab costs = 75% x ARV

you determine that you should purchase the property for no more than

purchase price = 75% x $500K – $60K = $327,500

The reason for targeting 75% of the ARV is to give you a buffer in case your rehab costs are higher than you estimated.

Assuming your borrowed money from a hard money lender to purchase the property at $327,500 and then you refinance it at $500K while cashing out 75% ($375,000), you could turn around pay off the hard money lender and even have some money left over ($47,500).

Following are some things that don’t typically add value for a rental

Granite countertops

Brazilian hardwood floors

High-end stainless steel appliances

Bay windows

Skylights

Hot tubs

Chandeliers

Following are some things that do typically add value for a rental

Roofs. If you add a new roof, appraisers tend to give you back the money you spent in property value.

Unfinished kitchens. An outdated kitchen is ugly but still usable. A partially demo’ed kitchen makes a house ineligible for financing and, therefore, much easier to buy with cash.

Drywall damage. Drywall damage makes a property ineligible for financing while also scaring away most home buyers. The good news? Drywall isn’t super expensive to repair.

Horrific landscaping. Overgrown vegetation frightens the competition but costs very little to repair. You don’t need a skilled landscaper to hack down overgrown landscaping, so a few hundred dollars will take you farther than you think.

Outdated bathrooms. I routinely completely remodel bathrooms for $3,000 to $5,000. Most bathrooms aren’t huge, so the material and labor costs come in low. This allows your house to compare to much nicer homes in the neighborhood with higher ARVs.

Too few bedrooms. Homes with more than 1,200 square feet but less than three bedrooms offer easy ways to add value. Adding a third or fourth bedroom helps it compare to much more expensive properties, increasing your ARV.

When purchasing properties using the BRRRR method, you normally can’t or don’t want to borrow money the traditional way (from a bank) because

banks often don’t want to finance non-livable properties

banks are slow and picky so sellers may be more interested in selling to all-cash buyers

“Subject-to” investing

“Subject-to” investing is purchasing a property subject to the existing mortgage that is already in place. Essentially, this is when an investor comes in and makes back payments for a homeowner who is behind on their payments, as opposed to the home falling into foreclosure. The original owner then deeds the property to the investor and moves out — often to downsize into a more affordable living space — while leaving the loan in place and the property under the investor’s ownership. It’s an investing strategy ideal for investors low on capital. Buyers in this situation aren’t formally assuming the loan. The terms of the original note stay the same, including the name in which the loan was purchased. And the buyer takes on the responsibility of making sure the mortgage is paid on time until it’s renovated and resell the property.

Section 8

Section 8 is a housing voucher program. It is the federal government’s major program for assisting very low-income families, the elderly, and the disabled to afford decent, safe, and sanitary housing in the private market.

Many landlords don’t like to offer Section 8 housing – possibly because renters who get Section 8 support may be less desirable. However, there are advantages to accepting Section 8 renters like

guaranteed on-time partial or full rent directly from the government

potentially higher rent

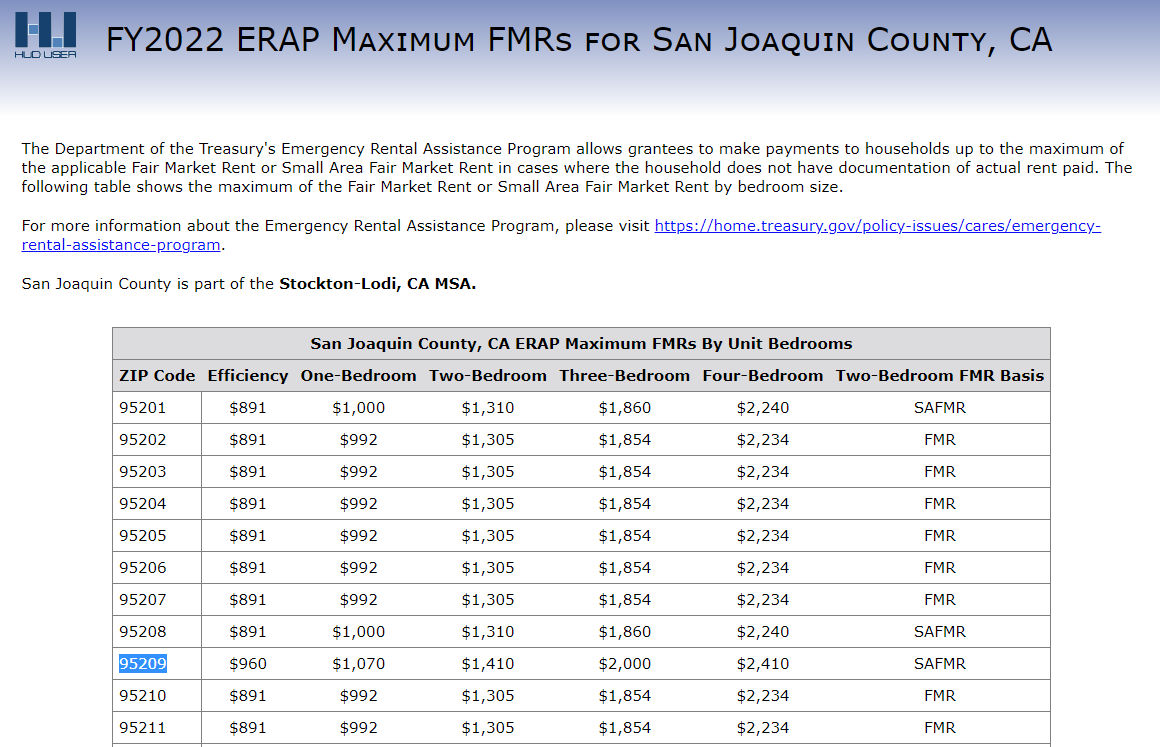

Many landlords get below-market rents for one reason or another. With Section 8, governments will pay rent for eligible tenants up to a certain amount based on zip code and number of bedrooms. The rent amount is called the Fair Market Rent (FMR). For example, one of my rentals in Stockton, California (San Joaquin County) is a triplex consisting of two 2-bedroom units and one 3-bedroom unit. It’s zip code is 95209. According to the table below, I could get

$1410 / month for each 2-bedroom unit

$2000 / month for the 3-bedroom unit

When I purchased the property, I inherited the tenants who were paying $1200 / month for a 2-bedroom unit and $1250 / month for the 3-bedroom unit. If the tenants leave, I could increase the rents to the FMR and accept Section 8 in case non-Section 8 renters are willing to pay the FMR. My total monthly rental income would increase from $3650 to $4820. That’s an increase of $1170 per month.

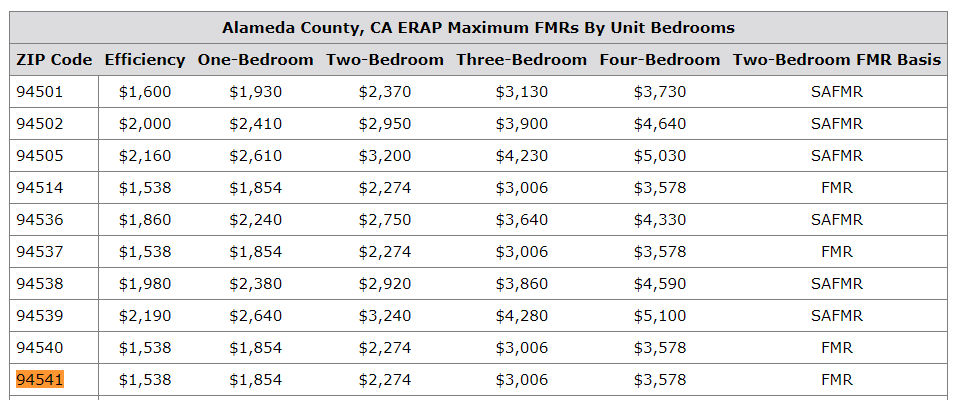

For my 3-bedroom rental in Hayward, California (Alameda County) / zip code 94541), the FMR is $3006 per month.

Add bedrooms

As you can see in the FMR charts above, homes with more bedrooms are more valuable as you can charge more rent. Some ways to add bedrooms is by

adding an addition to the existing property (this is expensive)

modifying walls in an existing property to make an extra bedroom (this is relatively cheap)

Let’s say you have a 1200+ sq ft house but it only has 2 bedrooms. Normally, you can easily fit 3 bedrooms in a 1200 sq ft house. The minimum area for a bedroom should be 120 sq ft. The average bedroom size is 132 sq ft. If you happen to have a super large bedroom, e.g. 250 sq ft, you can add a wall in between and turn a huge bedroom into two bedrooms.

Research

When deciding where to invest in a rental property, you often want to look at many factors such as population growth, income growth, appreciation of housing prices, and crime rates. You can find this information from City-Data.

Site-built homes are homes built on site. Most houses are site built. Manufactured homes are built in a factory and assembled on site. Manufactured homes are cheaper than site-built homes with excluding the cost of land. According to this article, the average cost per square foot for a manufactured home is $52 vs $115 for a site-built home. That a big difference.

If you buy a manufactured home and lease the land it’s on, you won’t be able to get a conventional loan / mortgage. Rather, you’d get a chattel loan which is like a loan for personal property (e.g. boat, airplane, etc) since the manufactured home is like personal property. If you buy a manufactured home and the land it is on, you can get a traditional loan / mortgage which offers better rates.

Depending on the cost of land, if might be cheaper to buy land and then buy a bunch of manufactured homes to put on it and then rent them all out rather than build a bunch of homes or a multi-family building on site.

AirBnB (short term) vs traditional (long term) renting

When you rent out your property, you have two options

long term (traditional)

short term (e.g. AirBnB)

Though long term rentals provide consistent long term cash flow, you can usually more more money from short term rentals, especially if you have a desirable property in a heavy tourist spot. For example, if you have a 3 bedroom home in downtown San Francisco (94103 zip code), the fair market rent is $4,120 per month. But, if you rent it out on a daily basis via AirBnB for $250 per night, you could get $250 x 30 = $7500 for one month. Of course, there are many other factors so you would need to consider all costs and expenses as well.

Increase your credit score as quickly and as high as possible (minimum 680)

Eliminate as much debt (credit cards, loans) as possible, e.g. monthly payments for a fancy car, etc.

Save as much money as possible (minimum $20,000)

Buy a used duplex (2-unit property) preferably with existing tenants where at least one tenant is paying the market rate for rent

Kick out the lower paying tenant and live in that unit

Slowly fix up the property as money becomes available and time permits to increase its value

After a few years, the home’s value will have appreciated and you will have more equity in the house. You can remain in that living situation or you can sell the duplex, take the profit, buy a single family residence or a better duplex or triplex.

Introductory Facts

Homeownership is the number one way for people to move from the lower class to the middle class and to build wealth.

People who own homes are almost always better off financially than people who always rent.

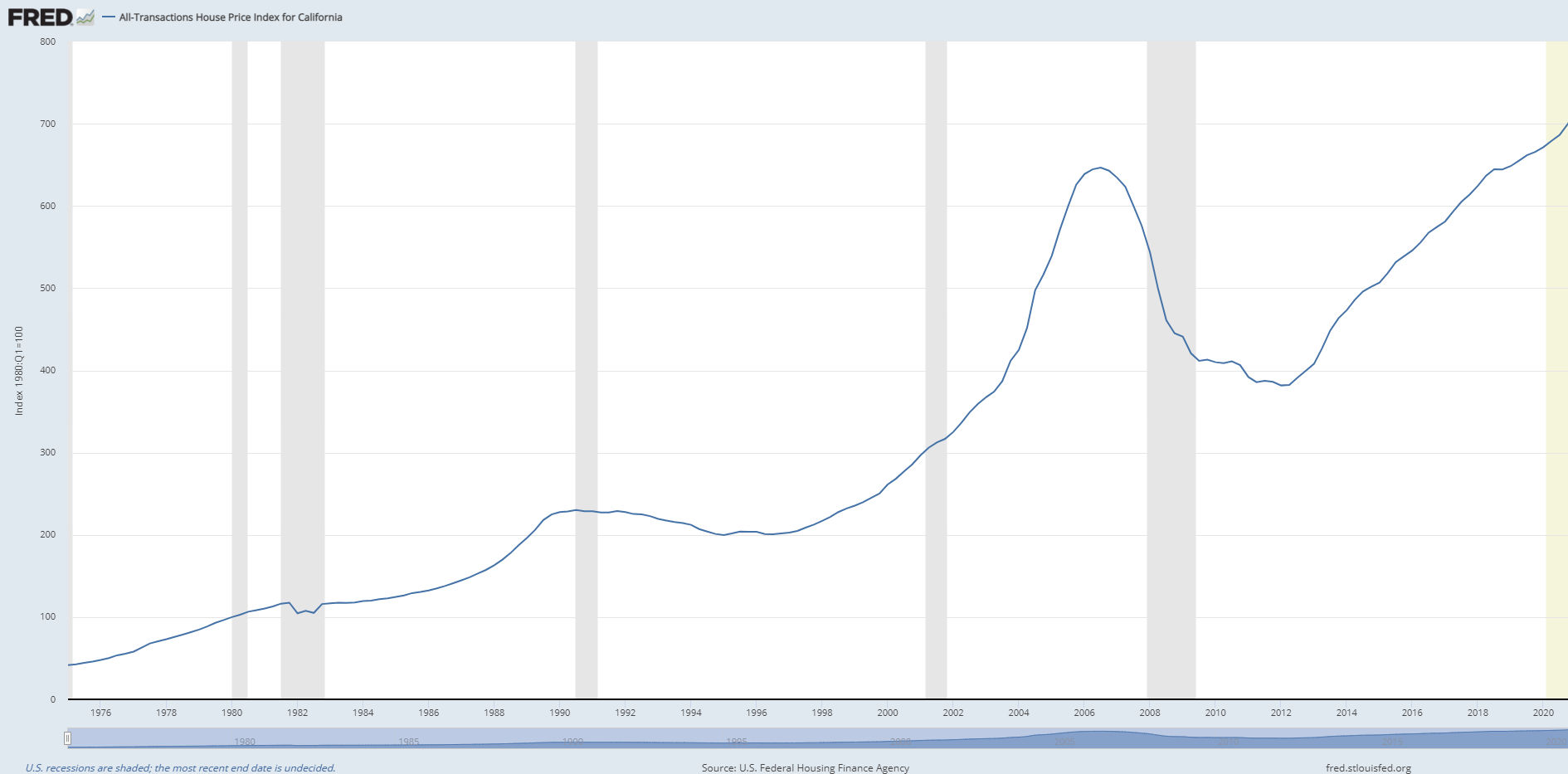

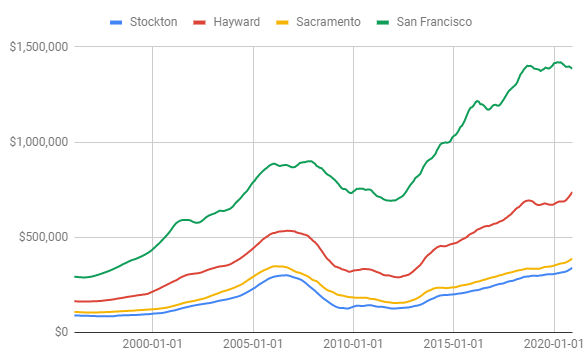

Real estate (e.g. houses) always increases in value over the long term (see graph below). The only exception was between 2008 – 2012 which was due to mortgage fraud and greedy banks which led to a global recession. It is now illegal to commit mortgage fraud which should prevent significant depreciation from occuring again.

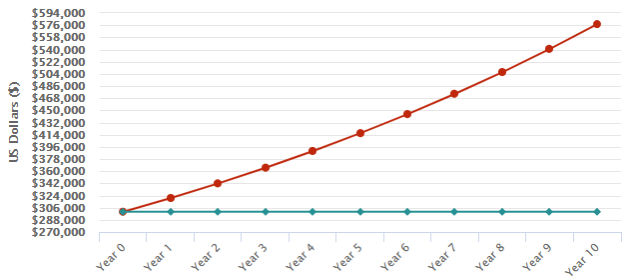

The average rate of appreciation of real estate in California is about 6.77% annually. That means if you buy a house for $300,000, then in one year, the value will have gone up by $300,000 x 6.77% = $20,310. You will have made $20,310 in one year for doing nothing but living in your own home. In 10 years, due to compounding appreciation, your home’s value will have increased by $277,582.

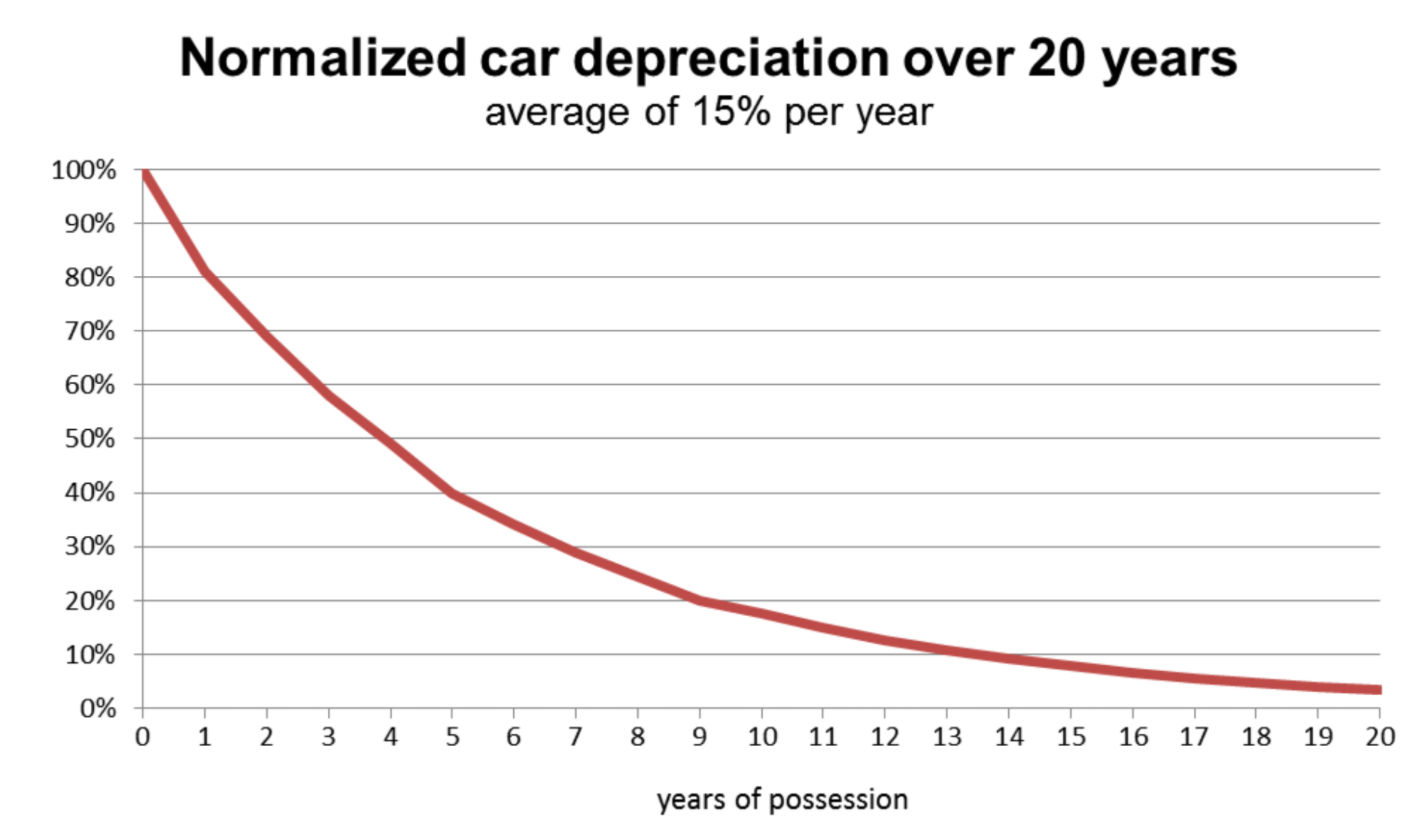

On the other hand, cars always lose value as time goes on. As a matter of fact, they lose an average of 15% per year.

When you rent, your entire monthly rent payment is spent and you get none of it back. However, when you buy a house and pay a mortgage, you get some of your mortgage payment back in the form of equity in the home. For example, if you borrow money from a bank for $300,000 at 3% interest fixed for 30 years (360 months) with a 3.5% down payment ($10,500), your monthly payments during the beginning and ending years will look like this:

Month

Principal & Interest

Principal

Interest

Principal Remaining

1

$1,221

$497

$724

$289,003

2

$1,221

$498

$723

$288,505

3

$1,221

$499

$721

$288,006

….

358

$1,211

$1,211

$9

$2,434

359

$1,211

$1,214

$6

$1,220

360

$1,211

$1,220

$3

$0 (loan paid off)

As you can see in the table above, in the beginning years, even though you pay $1221 per month for your mortgage, you are getting almost $500 back in the form of equity which is like a savings account but in the form of home value instead of at a bank. Your interest payments in the beginning are around $720 but it’s not money completely lost because mortgage interest is tax deductible which can lower your tax bill.

Rent always increases whereas mortgage payments never increase (on a fixed loan). As a matter of fact, nationally rent prices have increased an average of 8.86% per year since 1980, consistently outpacing wage inflation by a significant margin.

Between 2008 and 2020, annual wage increases for hourly employees maxed out at just above 3.5% which is less than both

the annual rate of rent increase (8.86%) since 1980

the annual rate of California home value appreciation (6.77%)

This means that your income growth is less than your housing expense growth. This also means that if you live month to month, as time goes on you will have less and less money as rent increases faster than your income.

Never buy a manufactured / mobile home. Though they are cheap, you will have to rent the land and if the landowner increases the rent on the land, you will most likely have no choice but to pay the increase since it would be difficult and very expensive to move your mobile home somewhere else. Even if you own land and buy a manufactured home to put on it, you will not be able to get a low-interest home loan to purchase a mobile home.

Condos and Townhouses

Condos and townhouses are cheaper than single family residences but you will have to pay an HOA (homeowner’s association) fee which can be very expensive, especially if there is a swimming pool. Also, you are limited in what you can do to your own home, e.g. you can’t paint the exterior, you can’t move walls, build additions, etc. You are better off not buying a condo or townhouse.

Single Family Residence

This type of home is ideal for a single family. However, unless your financial situation is good, it would be difficult to afford one.

This type of property is usually purchased by investors. However, anyone can buy one and live in one of the units and rent out the other units. Of course, the more units, the more expensive. Therefore, for first time homebuyers with a limited income, it is recommended to buy a duplex. The strategy recommended in this article is to live in one unit and rent out the other unit and let the rental income pay for some, most, or all of your mortgage.

Commercial (5 units or more)

This type of property is usually purchased by big investors or companies who have a lot of money. Most people cannot afford this type of property.

Number of Bedrooms and Bathrooms

Most houses come with either

2 bedrooms and 1 bathroom, a.k.a. 2/1

3 bedrooms and 2 bathrooms, a.k.a. 3/2

To keep costs low, focus on duplexes where each unit has 2 bedrooms and 1 bathroom.

Potential Rental Income

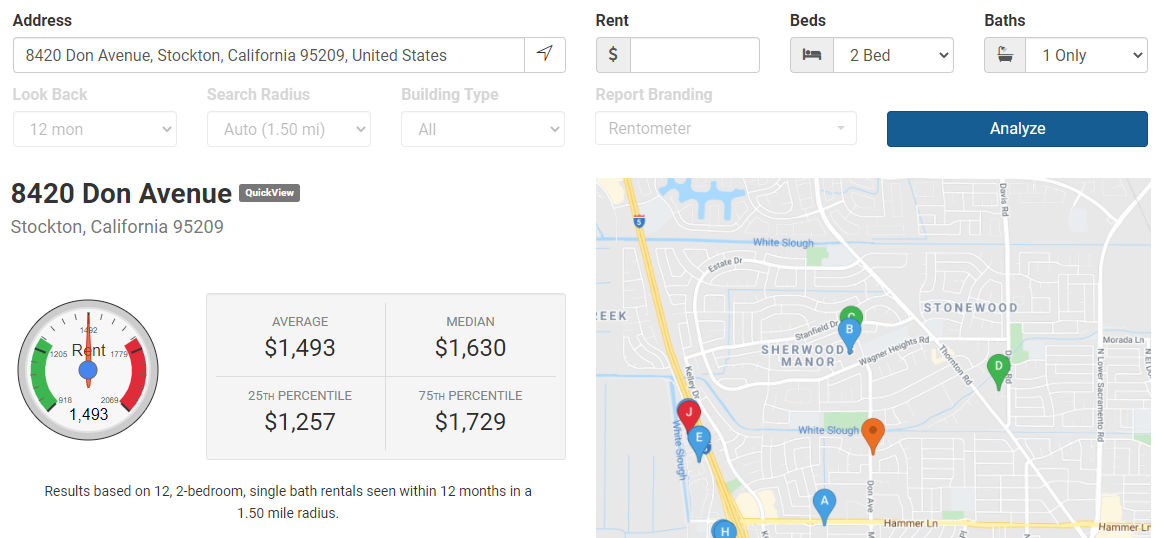

Since the recommended strategy is to buy a duplex and live in one unit and rent out the other, you need to know the potential rental income you will get to offset your mortgage expenses. To determine this, you can go to Rent-o-meter.

For example, the 2/1 duplex at 8420 Don Ave, Stockton, CA 95209 has an average rental income of $1493 for each unit. Therefore, if you buy this duplex, you could potentially get $1493 per month from your renter to help pay for some or all of your mortgage.

Determine Costs

As a first-time home buyer, you are entitled to the FHA First-Time Home Buyer program. This program allows you to borrow money to buy a house and only put a down payment of 3.5% as opposed to 20% for non-first-time home buyers and 25% for investors. However, if your down payment is less than 20%, you will have to pay private mortgage insurance (PMI).

For example, for a loan with the following numbers:

Purchase Price:

$300,000

Down Payment:

3.5% (10,500)

Loan Type:

30-year fixed (always choose this type)

Interest Rate:

3%

your total monthly mortgage-related expenses would be $1734.

However, since your rental income will be on average $1493, then your net monthly mortgage-related expenses will be

$1734 – $1493 = $241 per month

In other words, your monthly housing costs become ONLY $241 per month! But, that depends on

whether you can find a 2/1 duplex for $300,000

whether your credit score is good enough that you can get a loan with a 3% interest rate

whether you can actually rent out the other unit for $1493 per month

Interest Rates

Interest rates on your loan make a very big difference in your monthly mortgage expense and your lifetime loan cost. Due to the Covid-19 pandemic, the federal government lowered interest rates to almost zero to stimulate the economy and avoid a recession. In doing so, interest rates on home loans have been very low. As a matter of fact, interest rates have never been lower than now as indicated in the graph below.

Therefore, now is THE BEST TIME to get a home loan because the interest rates are at the LOWEST they have ever been. If you wait 2, 4 or 6 years from now, interest rates may go back up to 4 or 5% which means your monthly mortgage payments will be much higher.

Credit Score

Your credit score has a VERY BIG impact on the interest rate of your home loan. The higher your credit score, the lower the interest rate, and the cheaper your monthly mortgage expenses. Therefore, you want your credit score to be as high as possible.

To determine the interest rate you can get for different credit scores, you can go to Zillow > Home Loans > Mortgage Rates https://www.zillow.com/mortgage-rates/

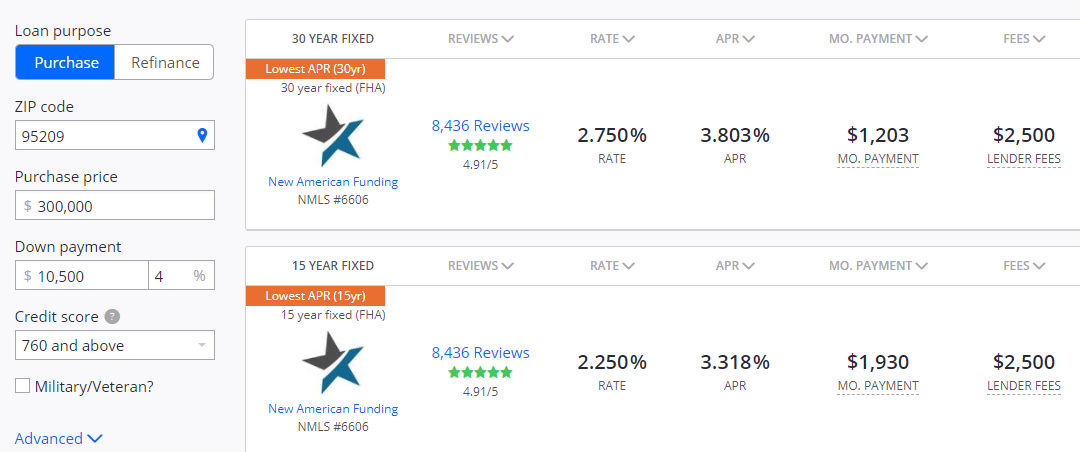

For example, for a loan with the following numbers:

Purchase Price:

$300,000

Down Payment:

3.5% (10,500)

you will find the following interest rates for different credit scores.

Credit Score

Interest Rate

560 – 599

No loans available

600 – 619

No loans available

620 – 639

No loans available

640 – 659

3.5%

660 – 679

3.25%

680 – 699

2.75%

700 – 719

2.75%

720 – 739

2.75%

740 – 759

2.75%

760 and above

2.75%

The rates above were valid on July 4, 2021. Interest rates change daily and throughout the day.

As you can see above, if your credit score is below 620, you can’t even get a loan. Also, the higher your credit score, the lower the interest rate.

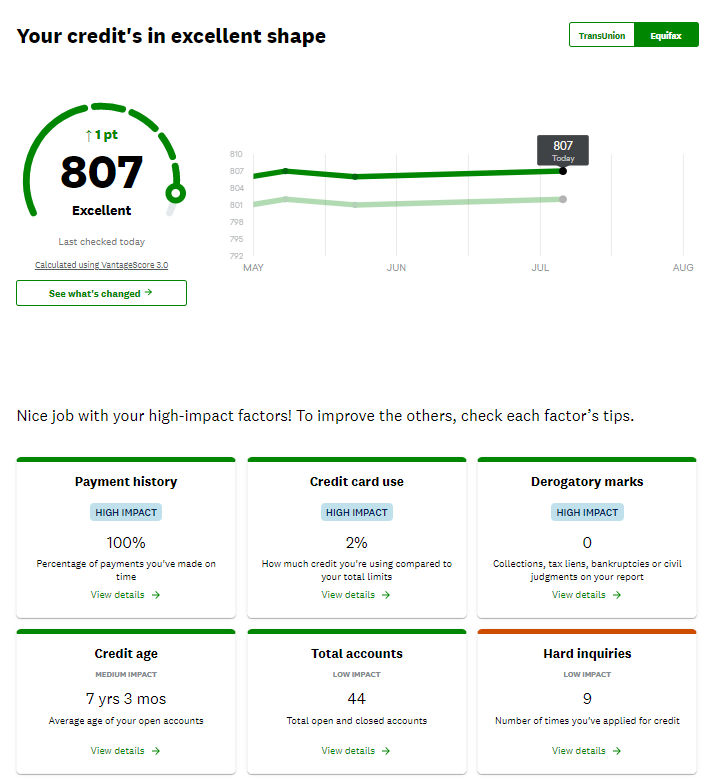

In order to improve your credit score, sign up for a free Credit Karma (https://www.creditkarma.com/) account, enter your information, and under “Credit Scores”, you will see your score for Transunion and Equifax followed by ways to improve each score.

Notice that there are 6 factors that affect your credit score, 3 of which are high impact.

Factor

Impact

Description

Payment History

High

Percent of payments you’ve made on time

Credit Card Use

High

How much credit you’re using compared to your total limits

Derogatory Marks

High

Collections, tax liens, bankruptcies or civil judgments on your report

Credit Age

Medium

Average age of your open account

Total Accounts

Low

Total open and closed accounts

Hard Inquiries

Low

Number of times you’ve applied for credit

From here on, we will assume you have increased your credit score to 680 and since interest rates change all the time, we’ll assume you can get a rate of 3%.

Interest Rate VS Loan Cost

Interest rates affect the cost of a loan and your monthly payments. Following are monthly mortgage costs and total loan costs for a $300,000 home loan at 30-year fixed at various interest rates.

Interest Rate

Monthly Mortgage Payment

Total Loan Cost Over 30 Years

2.5%

$1,190

$123,000

3%

$1,227

$151,000

3.5%

$1,307

$180,000

4%

$1,389

$209,000

4.5%

$1,474

$240,000

5%

$1,562

$271,000

5.5%

$1,652

$304,000

6%

$1,745

$337,000

As you can see, the interest rate makes a big difference in your monthly payment and loan costs. For example, for a 5% interest loan, you’ll be paying an extra $335 per month and an extra $120,000 over 30 years compared to a 3% interest loan for $300,000.

Mortgage-to-Income Ratio

Lenders require that in order to give you a home loan, your mortgage expenses (PITI) must not be more than 28% of your gross monthly income before taxes. PITI stands for

P = Principal

I = Interest

T = Taxes

I = Insurance

Let’s say that your total monthly income is $3000 per month before taxes. That means your PITI may be no more than 28% x $3000 = $840 per month. However, if you buy a duplex, then your total monthly income will increase by the rental income of, say, $1400 per month, which would bring your total monthly income to $4400. Therefore, your PITI for a duplex can be no more than $4400 x 28% = $1232 per month.

Debt-to-Income Ratio

Lenders also require that your total debt (including mortgage expenses) be no more than 43% of your gross monthly income before taxes. For example, if your monthly income is $3000 per month and your fancy car’s monthly payments are $350 per month and you are looking at buying a house with an estimated PITI expenses of $1000 per month, then your debt-to-income ratio is

Debt-to-Income Ratio = Debt / Income = ($350 + $1000) / $3000 = 0.45 or 45%

Since 45% is greater than 43%, you would not qualify for a loan.

Calculations

To help see all important numbers in one place, you can create a spreadsheet similar to the one below.

Loan Type

FHA – First-Time Home Buyer

Purchase Price

$300,000

Minimum Credit Score

680

Down Payment (%)

3.5%

Down Payment ($)

$10,500

Interest Rate

3%

Term

30 years fixed

Mortgage – Principal

$497

Mortgage – Interest

$724

Mortgage – Insurance (PMI)

$236

Property Tax

$170

Insurance

$105

Total Monthly Cost (PITI)

$1,732

Property Type

Duplex

Income – Work (Annual)

$60,000

Income – Work (Monthly)

$5,000

Income – Rental (Monthly)

$1,300

Total Gross Monthly Income

$6,300

Max Monthly Mortgage to Income (%)

28%

Max MonthlyMortgage Allowed ($)

$1,764

Max MonthlyTotal Debt to Income (%)

43%

Max MonthlyTotal Debt Allowed ($)

$2,709

Finding a House for Sale

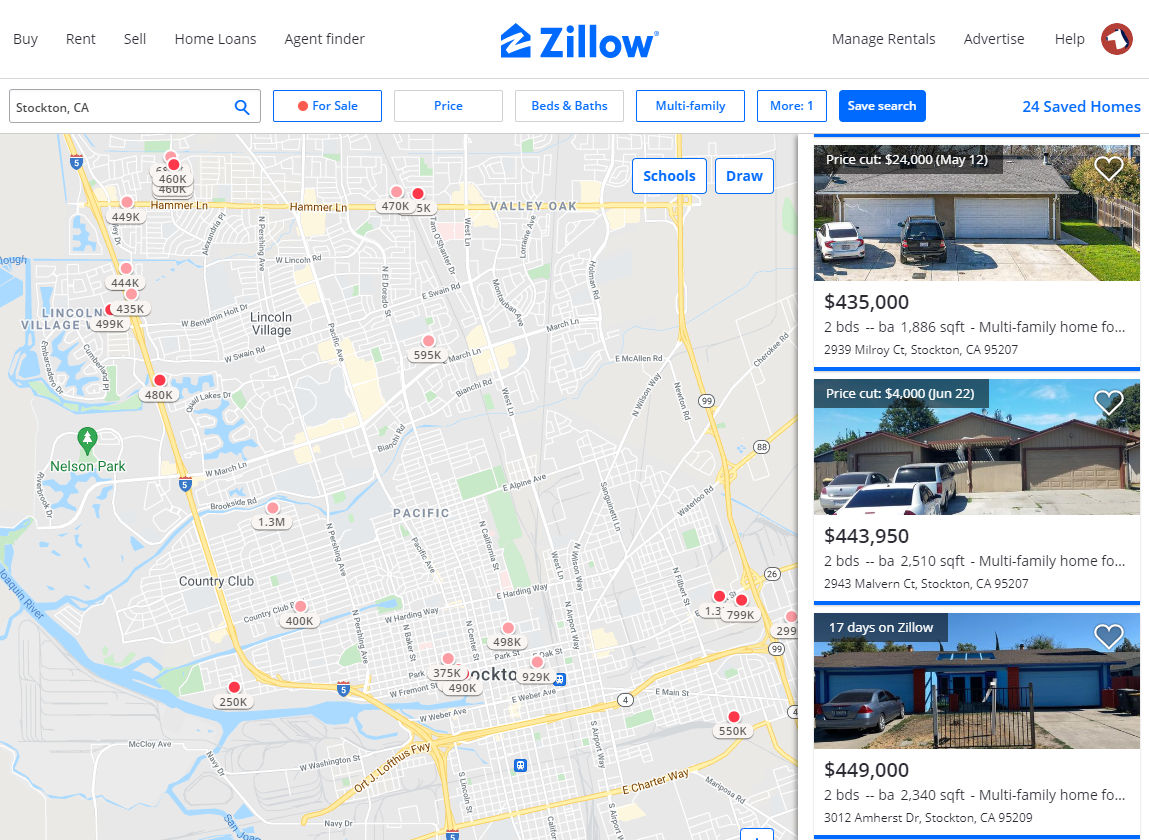

As mentioned above, the strategy is to buy a “used duplex”. To find these, go to Zillow and do a search.

The color is ugly but maybe that’s why no one has bought it. You can always paint it.

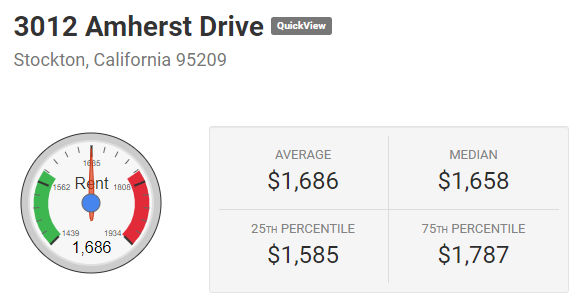

Rental Income:

This duplex may already have renters in both units. If you buy it, you can kick out the renter who is paying the lower amount and then live in that unit yourself.

If the duplex isn’t rented, you can check Rent-o-meter to determine average rent. After entering the address in www.rentometer.com, we see that the average rent is $1686.

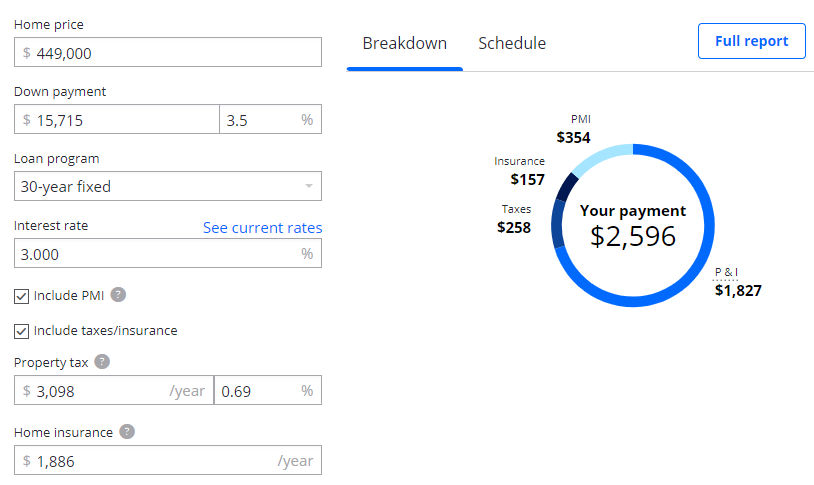

Mortgage Expenses:

Now, we need to calculate our mortgage expenses by going to Zillow’s mortgage calculator. For a loan with the following numbers:

Purchase Price:

$449,000

Down Payment:

3.5% ($15,715)

Loan Type:

30-year fixed (always choose this type)

Interest Rate:

3%

we get the following

This means that your total monthly housing expense will be $2596.

You net monthly housing expense becomes

$2596 – $1686 = $910 per month

$910 / month is very cheap for 2 bed 1 bath housing in Stockton and is much cheaper than renting. Also, as time goes on, the value of the property will go up on average 6.77% per year.

To reiterate, for the example above,

your net monthly housing expense would be

$910 per month

you need a down payment of

$15,715

you need a credit score of at least

680

you will need to pay for loan closing costs in the average amount of

$5000

Get Pre-Approved

Before making a move to buy a house, you increase your chances of success by first getting pre-approved. Don’t simply get pre-qualified because that doesn’t carry as much weight as a pre-approval. A pre-approval will verify your financial situation so you can feel confident you will be able to afford a house at a particular price. When the time comes, you can and should include your pre-approval letter with your house purchase offer so the sellers know you are serious and can afford to buy their house. When getting pre-approved, mention that you are interested in buying a duplex and renting out one of the two units so that the rental income is accounted for.

Since you are new to buying a house, you’ll want a real estate agent to guide and help you. You can easily find a real estate agent by searching Google for “Stockton real estate agent”.

Once you agree to work with an agent, you can tell them the type of property you want to buy (used duplex) and give them your pre-approval letter. You can then tell them which active listings on Zillow (or Redfin – www.redfin.com) you are interested in. The agent may also have pocket listings / off-market listings that meet your criteria.

Make an Offer

Once you decide to put an offer on a house, you need to decide how much you are willing to pay for it. In a hot market, there could be competition driving up prices. If Zillow estimates the house to be worth $360,000 and the seller is asking for $360,000, then you may want to offer $370,000 to beat the competition. Note, however, that in a hot market, values can go up quickly. I offered $30,000 above the asking price and I still got outbid by someone who bought the property for $40,000 above asking.

Your agent can help you determine the value of the house and draft up a purchase offer. You will review the offer letter for accuracy and then sign it. Your agent will then submit the offer to the seller’s agent and wait for a response. If the seller accepts your offer, then you’re locked in and the seller cannot change their mind and sell to someone else.

NOTE:

For tips on buying a house, read my article titled House-Buying Tips.

For strategies on competing with other buyers in a hot market, read my article titled House-Buying Strategies.

Get a Loan and Fire Insurance

Home Loan

I have not purchased a home using the FHA First-Time Home Buyer program. However, I have found LoFi Direct to offer very competitive rates for home loans.

For fire insurance, I recommend using a broker to shop around and find a deal for you. They usually can offer lower rates than if you go directly to the large insurance companies. Just search Google for “home insurance broker”.

Close Escrow

Once everything is in order, you will “close escrow” which means you finalize the deal. It takes about one month from when your offer is accepted to when you close escrow. Once you close escrow, you become the legal owner of the property and you can move in. Just make sure you pay your mortgage payments and property tax so the lender and government don’t take your house from you.

Many, if not most, people aren’t experienced with buying and selling a house. For that reason, they hire a real estate agent. However, once you’ve bought one or two houses, you’ll realize it’s not that hard. 50 years ago, when online MLS sites like Zillow didn’t exist, having an agent find a house for you was useful. However, nowadays, buyers can get notified instantly when a house matching their criteria comes on the market. This reduces the value of having an agent. Furthermore, in California, real estate agents get a 3% commission. Even though this is paid by the seller, in certain situations the buyer pays by having to offer a higher purchase price. By buying a house without an agent, the seller doesn’t have to pay 3% commission to a buyer’s agent which means you can offer a lower purchase price than other buyers who have an agent. For a $500,000 house, this can save you $15,000.

Below are steps to buy a house without an agent.

1. Get a pre-approval letter

Assuming you will be borrowing money to buy the house, as for most people, you need a pre-approval letter. This is for 2 reasons:

Find out how much of a house you can afford

Prove to the seller you can actually afford to buy their house

To get a pre-approval letter, you can submit an application to purchase a home on Zillow Home Loans. You can do the same at LoanDepot.com which is reportedly the second-largest non-bank provider of direct-to-consumer loans in the United States. Another option is to compare lenders based on interest rate offered. By filling out some information on Zillow’s Mortgage Rates page, you’ll be presented with multiple lenders and interest rates. You can then pick a lender, get in contact with them, and ask for a pre-approval letter at the rate they advertised. Here’s an example pre-approval letter.

A pre-approval letter is different from a prequalification letter. With a pre-approval, your financial situation is verified and your credit score is checked.

2. Search for a house

The easiest thing to do is search Zillow. You can also search Redfin, Trulia, and official MLS websites.

Appraisal

Note the automated estimates, e.g. Zestimate and Redfin estimate. They will give you a good idea of the value of the property. However, don’t assume they are correct. Sometimes, their algorithms use uncomparable properties to determine value leading to incorrect values, e.g. comparing a multifamily property or condo to a single-family property. You can see the properties each website uses to determine a particular value. If they don’t make sense, you can calculate the price per sq ft of similar properties recently sold and come up with a more accurate estimate. See an example. Based on the pictures, neighborhood and estimate, think of how much you’d pay for the property.

Tips

See my post on house-buying tips to learn more about certain things to watch out for.

RPA – California Residential Purchase Agreement and Joint Escrow Instructions – 4 Pack

This form is the main form used for making an offer. It includes

(AD) Disclosure Regarding Real Estate Agency Relationship

(BIA) Buyer’s Inspection Advisory

(PRBS) Possible Representation Of More Than One Buyer Or Seller

(WFA) Wire Fraud Advisory

Price

$170.98 (CAR Member Price)

$341.95 (CAR Non-Member Price)

Other useful forms

TDS – Real Estate Transfer Disclosure Statement The property disclosure statement is required by law in most residential sales transactions in California. It includes Seller’s mandatory disclosure of specified items and any known adverse material conditions, as well as sections for Seller’s and Buyer’s agents to comply with diligent visual inspection requirements.

BCO – Buyer Counteroffer Counteroffer form to be used when a buyer initiates a counter offer.

SCO – Seller Counteroffer Counteroffer form to be used when a seller initiates a counter offer.

WOO – Withdrawal of an Offer This form is used to revoke an offer or counter offer before the document has been accepted.

Important Terms of Purchase Offer

The standard California residential purchase offer form is written to protect buyers by default. Following are some key clauses.

You will submit the purchase offer to the seller’s agent or, if it’s an FSBO (for sale by owner) listing, then to the seller directly.

Since you are submitting your purchase offer yourself without an agent, you should make it clear that your offer will not require the seller to pay a commission to a buyer’s agent. For a 3% rate, the seller could save $15000 on a $500,000 purchase offer. Below is an example cover letter for this purpose.

Note to Seller:

This offer is from a buyer with no agent. I (the buyer) am representing myself. As such, acceptance of this offer by you (the seller) would save you from having to pay a commission to a buyer’s agent. Since my offer is for $390K, assuming a commission rate of 3%, my offer would save you $390K x 3% = $11,700, and your total commission expense would only be $11,700 to your own agent (seller’s agent). Your net proceeds (excluding other expenses) would be $390K – $11700 = $378300 as shown below.

My Offer

Commission to Seller’s Agent

Commission to Buyer’s Agent

Seller’s Net Proceeds

Purchase Price

3%

0%

(excluding other expenses)

$390,000

$11,700

0

$378,300

If there is another offer above $390K but below $403K and that offer includes a buyer’s agent, then you’d have to pay 6% commission (3% for each agent). In this case, my offer will net you higher proceeds as you can see from the table below.

Other Offers

Commissionto Seller’s Agent

Commission to Buyer’s Agent

Seller’s Net Proceeds

Purchase Price

3%

3%

(excluding other expenses)

$391,000

$11,730

$11,730

$367,540

$392,000

$11,760

$11,760

$368,480

$393,000

$11,790

$11,790

$369,420

$394,000

$11,820

$11,820

$370,360

$395,000

$11,850

$11,850

$371,300

$396,000

$11,880

$11,880

$372,240

$397,000

$11,910

$11,910

$373,180

$398,000

$11,940

$11,940

$374,120

$399,000

$11,970

$11,970

$375,060

$400,000

$12,000

$12,000

$376,000

$401,000

$12,030

$12,030

$376,940

$402,000

$12,060

$12,060

$377,880

$403,000

$12,090

$12,090

$378,820

To conclude, my offer of $390K will net you a higher profit than any other offer up to $402K.

5. Do a home inspection

Inspections aren’t usually required by your mortgage lender, but they can reveal hidden issues that the seller might not know about. A typical home inspection covers surface-level elements of the home, including its plumbing, structure, heating system, and more.

You can search for home inspectors on Zillow’s website or Google.

Expect to pay at least $400 for a home inspection from a reputable company on an average 2,000-square-foot home.

If the inspection reveals an issue with the home, there are a few ways you can negotiate with the seller.

Ask For Repairs You can ask the seller to repair any problems with the home before closing.

Ask For Reimbursement You can ask the seller to reimburse you for the cost of repairs. This guarantees that you’ll get work from a quality contractor because you choose the professional. However, you might have trouble getting a seller to agree to pay a bill if they don’t know how much it will be.

Ask For A Discount You can ask the seller for a reduction of the sale price if there are significant repairs that need to be made.

Cancel The Sale If you can’t reach a solution with the seller and the issues are a deal-breaker for you, you can always cancel the sale.

7. Finalize financing and close

When you reach an agreement with the seller, it’s time to close on the loan.

Appraisal

Your lender will likely require you to pay for an appraisal. You’ll pay up to $500 and the lender will choose the appraiser. They do this to protect themselves so that if you default on the loan, they can reduce their losses. The appraisal report will also protect you so that you are not overpaying for the property. If the property isn’t worth what you’re offering, you can negotiate to lower the purchase price. Or, you can put a larger down payment if you really want the house.

Your lender will first give you a loan estimate. As soon as the appraisal and underwriting are cleared, your lender will send you a closing disclosure. Your loan estimate and closing disclosure tell you about the terms of your loan, your closing costs, your interest rate, and more. Compare the loan estimate to the final closing disclosure to ensure everything is as expected. If everything looks good, contact your lender and schedule your closing. The examples below are for a refinance but they are similar for a purchase.

Zillow provides housing and rental market data on the Research page. Using this data, I created the table below that shows the top 100 most populated cities in America along with their typical house value and monthly rent cost. GRM stands for Gross Rent Multiplier. GRM = Property Purchase Price / Annual Rental Income. It gives you an idea of how many years it will take for your rental income to pay for the cost of the property. It’s often used to compare investment properties. For example, if you buy a triplex for $490,000 and your monthly rental income from the 3 units is $3400, then

GRM = $490,000 / ($3400 x 12 months) = 11.3 years.

Note:

Houses in Texas are cheap but property taxes are some of the highest in the country. But then again, Texas has no state income tax.

Houses in Florida are cheap but the weather is humid and there are often hurricanes.

Chicago is cheap but it gets very cold during the winter there.

The weather is California is GREAT but houses are expensive.

Modular and therefore can add modules that offer different / better features

HDR (high dynamic range) for better image quality

More advanced desktop editing software

Cons:

Modular and therefore can be a hassle to have to switch modules, especially quickly in order to capture a moving target

GoPro Max

Pros:

Easy to use without having to assemble modular parts

Cons:

No HDR (high dynamic range)

Desktop editing software not as powerful as the Insta360 Studio

Insta360 One X2

Pros:

Small

HDR (high dynamic range) for better image quality

Ricoh Theta SC2

After testing the GoPro Max, Insta360 One X2, and the Ricoh Theta SC2, it clear that the Insta360 One X2 is the better camera.

Virtual Reality / 3D Panorama Software

Marzipano

Marzipano is free and open source. You can use the Marzipano tool to quickly upload 360 photos and then download a complete website with all code to host yourself. However, you can only zoom out so much as shown in the screenshot below.

Kuula

Kuula lets you upload 360 photos and embed a 360 viewer of your photos on your website. You can also zoom out much more than with Marzipano as shown in the screenshot below.

You can then take a screenshot of the zoomed out 360 photo which doesn’t show very warped and curved lines.

Metareal

Metareal is a great alternative to MatterPort. You can create floorplans as well and pay a nominal fee to have Metareal convert your 360 photos into virtual tours for you.

Photoshop

In Adobe Photoshop, you can import a 3D panorama photo

In the lower left corner, when you have the white grid enabled, you will see orbit, pan and dolly buttons to move the image around.

Under Properties, you can adjust the Vertical FOV (Field of View) to zoom in and out.

GoPro Player Desktop App

The GoPro Player desktop app will also open 360 photos and let you rotate and zoom in and out. But, unlike Photoshop and Kuula, you’ll get a fisheye view as shown below.

Google Photos Mobile App

The Google Photos mobile app has a Panorama feature but you have to move your camera horizontally or vertically to capture create the panorama. It’s not a full 360 degree panorama but it does support scrolling in Google Photos.

Insta360 Studio

The Insta360 Studio desktop app is definitely better than the GoPro Player desktop app. It’s got more features and is intuitive to use.

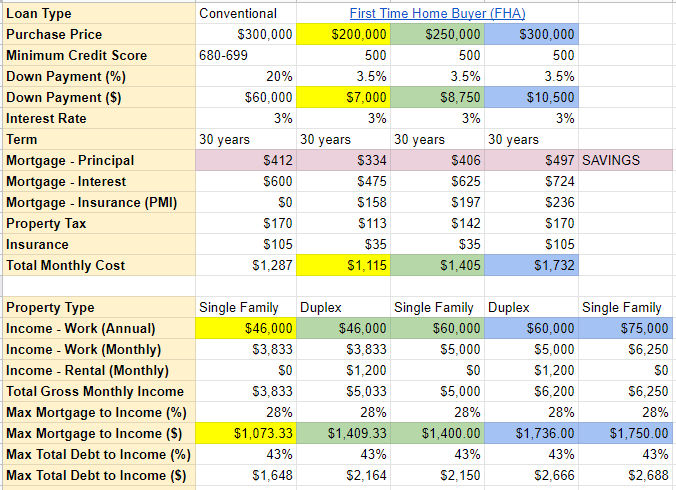

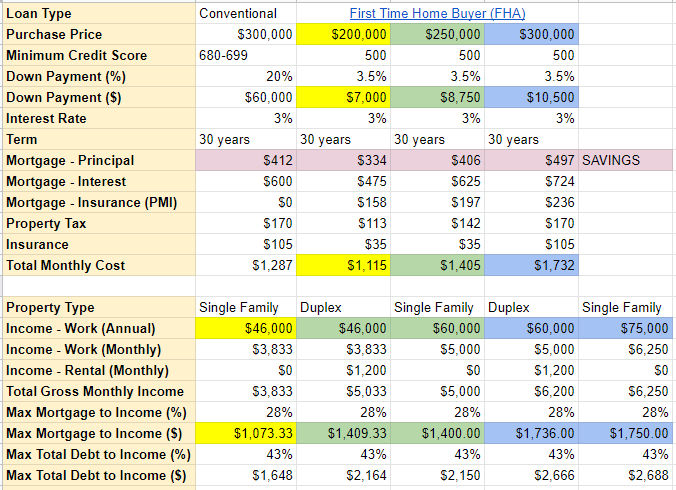

It is January 2, 2021 and the previous year has surprised everyone. Analysts predicted home prices to fall due to the global Coronavirus pandemic but in the US, home prices surged despite millions of Americans losing their jobs.

At this time, the cost to rent an apartment in Hayward, California is

~$1600 / month for a 1 bedroom apartment

~$1800 / month for a 2 bedroom apartment

Now, let’s see how much it costs to buy a house with the following assumptions:

Buyer credit score is 680

Buyer has never purchased a home before

The top half of the table below shows 4 different loan scenarios.

Conventional loan requiring a 20% down payment and a purchase price of $300K

FHA (first time home buyer) loan requiring a 3.5% down payment and mortgage insurance for a purchase price of $200K, $250K, and $300K

At this time, Zillow indicates that one with a credit score between 680 and 699 can get a 30 fixed rate mortgage for 3%.

For a conventional loan of house costing $300K, if one has $60K for the 20% down payment, their monthly mortgage including principal, interest, taxes, and insurance (PITI) would be $1287. This is far below the the cost to rent a 1 bedroom apartment in Hayward, CA.

For the FHA loan, one would only need a 3.5% down payment but they’d have to pay mortgage insurance. The total monthly mortgage-related expenses (PITI) are

$1155 for a $200K purchase price

$1405 for a $250K purchase price

$1732 for a $300K purchase price

These costs are all lower or equal to the cost to rent in Hayward, CA. The problem, however, is house prices in Hayward are very high. The closest large city with house prices between $200 and $300K is in Stockton, CA, e.g.

Now, just because the monthly mortgage expenses are lower than the cost to rent, that doesn’t mean one would qualify for a loan. Lenders require

mortgage expenses (PITI) to be no more than 28% of one’s gross monthly income before taxes

total debt (including mortgage expenses) to be no more than 43% of one’s gross monthly income before taxes

The bottom half of the table below shows different income scenarios as follows:

Having a gross annual income of $46K and buying a single family home

Having a gross annual income of $46K, buying a duplex and renting one unit out for $1200 per month

Having a gross annual income of $60K and buying a single family home

Having a gross annual income of $60K, buying a duplex and renting one unit out for $1200 per month

Having a gross annual income of $75K and buying a single family home

In these scenarios, we find that:

If you have a gross annual income of $46K and

you buy a single family home, then your maximum mortgage expenses can be $1073.33. In this case, you can buy a house for $200K (yellow cells)

you buy a duplex and rent out one unit for $1200 per month, then your maximum mortgage expenses can be $1409.33. In this case, you can buy a duplex for $250K (green cells)

If you have a gross annual income of $60K and

you buy a single family home, then your maximum mortgage expenses can be $1400. In this case, you can buy a house for $250K (green cells)

you buy a duplex and rent out one unit for $1200 per month, then your maximum mortgage expenses can be $1736. In this case, you can buy a duplex for $300K (blue cells)

If you have a gross annual income of $75K and

you buy a single family home, then your maximum mortgage expenses can be $1750. In this case, you can buy a house for $300K (blue cells)

But Stockton is too far from Hayward!

Assuming you currently live and work in or around Hayward, then it’s true that Stockton is a bit far. According to Google Maps, it’s about a 1 hour drive in no traffic between the two. However, according to this article, many people who work in the Bay Area can no longer afford local housing and have moved to Stockton and commute.

What if I save money and buy a house later?

If you make $46K a year and rent an apartment for $1800 per month, you probably won’t have much left over to save. And, even if you could save $100 per month, house value appreciation could outpace your savings. When you buy a house, some of your monthly payments go towards paying down the principal on your home loan. That, in effect, is a form of savings (pink cells in table) but in the form of equity in the house rather than cash in the bank. After a few years, your wealth could grow in 2 ways:

Appreciation of house value

Equity in paying down the principal on your home loan

You could then potentially sell the house and use the proceeds to put 20% down on another house thereby reducing your monthly mortgage payments even further.

What if the house value drops?

According to this article, recessions typically occur around every 10 years but they don’t necessarily cause house prices to flatten or drop. Housing busts typically occur every 18 years. The last housing crisis was in 2008 so the next one may occur in 2026 (5 years from now).

House Value Trends

Using data from Zillow Research Data, we can create a custom graph showing house value trends like the one below.

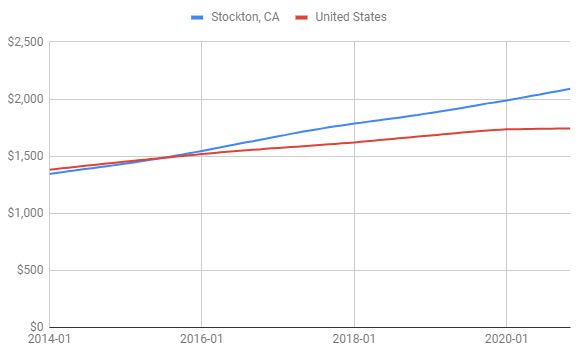

Similarly, we can chart the rent cost over time. Below is an example using US and Stockton, CA rents.