Following are some ways once can finance the purchase of real estate.

Conventional loan (mortgage)

Most people who buy real estate get a conventional loan and pay a mortgage for 30 years. They typically put a 20% down payment. Most banks, however, don’t want anything to do with a high-risk property that needs work. So to qualify for a conventional loan from a bank, a buyer / investor will first need to get the property up to a living standard.

Private lender

Private lenders are simply individuals, not businesses, who are willing to loan you money, e.g. family and friends. Sometimes, parents may gift their kids the down payment required to purchase a property but behind the scenes, make an agreement so that the kids pay back the money over a period of time. This is necessary since banks / lenders most likely would not allow the borrower to have multiple loans. Borrowing money in this way is easy because it doesn’t involve credit checks, appraisals, underwriting, etc.

Hard money lender

Hard money lenders are companies or funds that will loan you the money for a fee (interest). This process requires credit checks and includes underwriters who also determine the property’s value. Hard money lenders charge higher interest rates and the loans are for a much shorter period of time. The average is 6 months. Unlike private lenders, who often just trust that you’re making a good investment, hard money lenders will double check that your investment is reasonably sound since otherwise, they could lose money if you default.

House hack

House hacking is buying a property and renting a portion of it out to cover your expenses. You could be a 3 bedroom house and rent out 2 of the bedrooms. Or, you could buy a multifamily property (duplex, triplex, etc), and rent out the other units. In doing this, you significantly reduce your monthly expenses because you’ll have tenants paying for a big portion of your mortgage / loan.

Home equity loan

If you already own a home and have equity in it, then you could borrow money against it.

- You borrow money against equity in your existing home

- The interest rate is typically fixed

- If you still have a mortgage, a home equity loan would be a second mortgage behind your first mortgage

- You get the entire amount of the loan at once upon closing

HELOC

HELOC stands for Home Equity Line of Credit. If you already own a home and have equity in it, then you could borrow money against it.

- You borrow money against equity in your existing home

- The interest rate is variable and tied to prime

- If you still have a mortgage, a home equity loan would be a second mortgage behind your first mortgage

- You get to draw money from the line of credit multiple times (like a credit card)

Refinance

If you have a mortgage on your home, you can refinance the loan to replace it with another one. You typically do this if interest rates have dropped thereby lowering your monthly mortgage payments.

Cash-out refinance

This is like a regular refinance except you also get cash from the equity in your home. You could then use that cash to pay for purchasing another property, for example. The maximum cash you can get is 80% of the value of the home.

Flip

To flip real estate means to buy a fixer upper, renovate it, then turn around and sell it for a profit. houses. Can be mobile homes, single family, multifamily, etc.

Add Square Footage

Residential real estate (including multi-family properties with 4 or less units) is often valued by square footage. One strategy to increase the value of a property is by enlarging it, e.g. by adding bedrooms. If you know how to do this cost effectively, e.g. if you know how to do some or all of it yourself, you can add value and sell the property for a profit. Of course, this will depend a lot on where you live. For example, if you live in the Bay Area where the cost per square foot is very high, adding an addition to an existing property could be worth it.

BRRR method

BRRRR stands for “buy, rehab, rent, refinance, repeat.” With this real estate investment lifecycle, you could

- buy a property (whether using a conventional loan from a bank, HELOC, private loan or a hard money loan)

- rehab the property to increase it’s value (like fixing up a fixer upper)

- rent out the property. Banks rarely want to refinance a property that isn’t occupied, so renting your house comes first.

- refinance the property. This is actually a cash-out refinance using a conventional loan from a bank and get cash back. In this step, you would expect the property to appraise for much more than your purchase price because you rehabbed the place. The bank would require an appraisal. Once the appraisal is done, you could get 20% of the appraised value in cash and finance the remaining 80%. You may want to get pre-approved for the AVR before buying the property to ensure you will be able to refinance the property when the time comes.

- Waiting for seasoning

Many conventional and portfolio lenders require properties to “season” first. Seasoning means you’ll need to wait between six and 12 months before refinancing. If you’re using a private or hard money lender, it’s imperative to calculate exactly how much this period of time will cost you.

- Waiting for seasoning

- repeat. Using the cash you got from step 4, you would use it towards buying another property so you could repeat the entire process all over again

The key to the success of the BRRRR method is to

- buy properties under market value

- never investing more than 75% of the property’s after-repair value (ARV)

- ensure that you can rent the property at a rate that will cover your expenses by looking a rental comps

Let’s say that you find a property that is in disrepair. It’s been on the market for a while because no one wants to fix it up. You determine that the repairs are mostly or all cosmetic and not structural (e.g. foundation, etc). You estimate the value of the property after you repair it to be $500K based on nearby comparables, Zillow Zestimates, etc. You also estimate it would cost you $60K to fix it up. Therefore, based on the following equation

purchase price + rehab costs = 75% x ARV

you determine that you should purchase the property for no more than

purchase price = 75% x $500K – $60K = $327,500

The reason for targeting 75% of the ARV is to give you a buffer in case your rehab costs are higher than you estimated.

Assuming your borrowed money from a hard money lender to purchase the property at $327,500 and then you refinance it at $500K while cashing out 75% ($375,000), you could turn around pay off the hard money lender and even have some money left over ($47,500).

Following are some things that don’t typically add value for a rental

- Granite countertops

- Brazilian hardwood floors

- High-end stainless steel appliances

- Bay windows

- Skylights

- Hot tubs

- Chandeliers

Following are some things that do typically add value for a rental

- Roofs. If you add a new roof, appraisers tend to give you back the money you spent in property value.

- Unfinished kitchens. An outdated kitchen is ugly but still usable. A partially demo’ed kitchen makes a house ineligible for financing and, therefore, much easier to buy with cash.

- Drywall damage. Drywall damage makes a property ineligible for financing while also scaring away most home buyers. The good news? Drywall isn’t super expensive to repair.

- Horrific landscaping. Overgrown vegetation frightens the competition but costs very little to repair. You don’t need a skilled landscaper to hack down overgrown landscaping, so a few hundred dollars will take you farther than you think.

- Outdated bathrooms. I routinely completely remodel bathrooms for $3,000 to $5,000. Most bathrooms aren’t huge, so the material and labor costs come in low. This allows your house to compare to much nicer homes in the neighborhood with higher ARVs.

- Too few bedrooms. Homes with more than 1,200 square feet but less than three bedrooms offer easy ways to add value. Adding a third or fourth bedroom helps it compare to much more expensive properties, increasing your ARV.

When purchasing properties using the BRRRR method, you normally can’t or don’t want to borrow money the traditional way (from a bank) because

- banks often don’t want to finance non-livable properties

- banks are slow and picky so sellers may be more interested in selling to all-cash buyers

“Subject-to” investing

“Subject-to” investing is purchasing a property subject to the existing mortgage that is already in place. Essentially, this is when an investor comes in and makes back payments for a homeowner who is behind on their payments, as opposed to the home falling into foreclosure. The original owner then deeds the property to the investor and moves out — often to downsize into a more affordable living space — while leaving the loan in place and the property under the investor’s ownership. It’s an investing strategy ideal for investors low on capital. Buyers in this situation aren’t formally assuming the loan. The terms of the original note stay the same, including the name in which the loan was purchased. And the buyer takes on the responsibility of making sure the mortgage is paid on time until it’s renovated and resell the property.

Section 8

Section 8 is a housing voucher program. It is the federal government’s major program for assisting very low-income families, the elderly, and the disabled to afford decent, safe, and sanitary housing in the private market.

Many landlords don’t like to offer Section 8 housing – possibly because renters who get Section 8 support may be less desirable. However, there are advantages to accepting Section 8 renters like

- guaranteed on-time partial or full rent directly from the government

- potentially higher rent

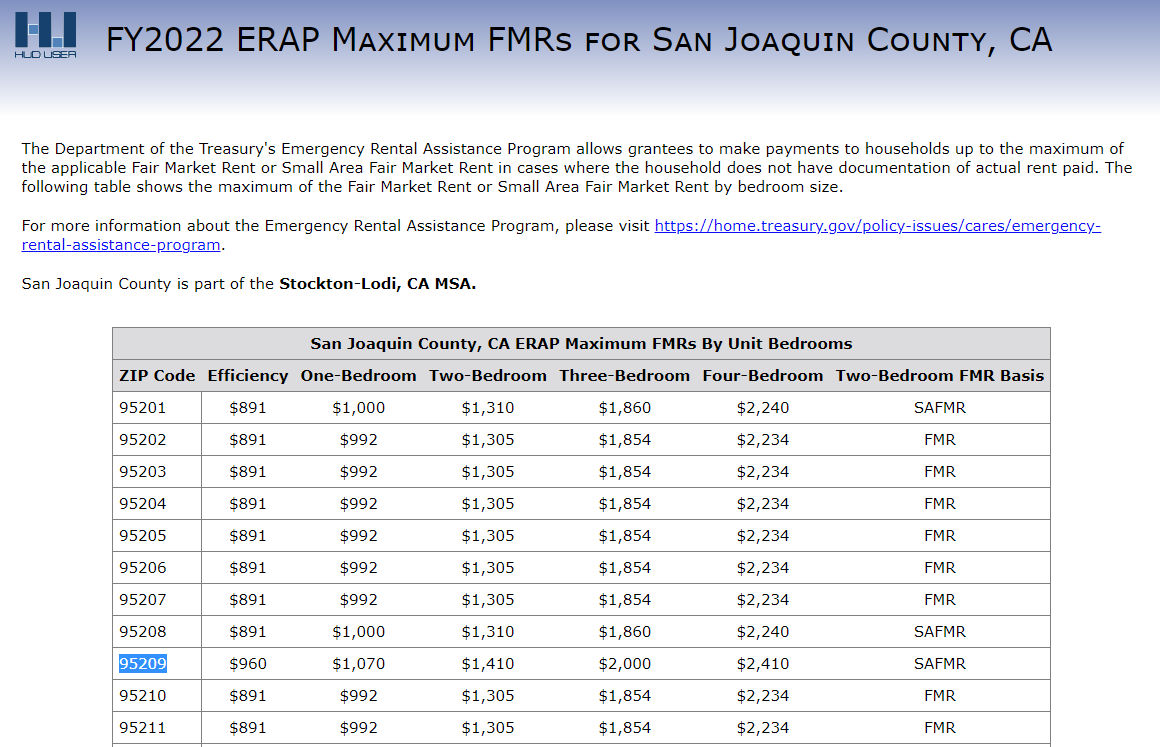

Many landlords get below-market rents for one reason or another. With Section 8, governments will pay rent for eligible tenants up to a certain amount based on zip code and number of bedrooms. The rent amount is called the Fair Market Rent (FMR). For example, one of my rentals in Stockton, California (San Joaquin County) is a triplex consisting of two 2-bedroom units and one 3-bedroom unit. It’s zip code is 95209. According to the table below, I could get

- $1410 / month for each 2-bedroom unit

- $2000 / month for the 3-bedroom unit

When I purchased the property, I inherited the tenants who were paying $1200 / month for a 2-bedroom unit and $1250 / month for the 3-bedroom unit. If the tenants leave, I could increase the rents to the FMR and accept Section 8 in case non-Section 8 renters are willing to pay the FMR. My total monthly rental income would increase from $3650 to $4820. That’s an increase of $1170 per month.

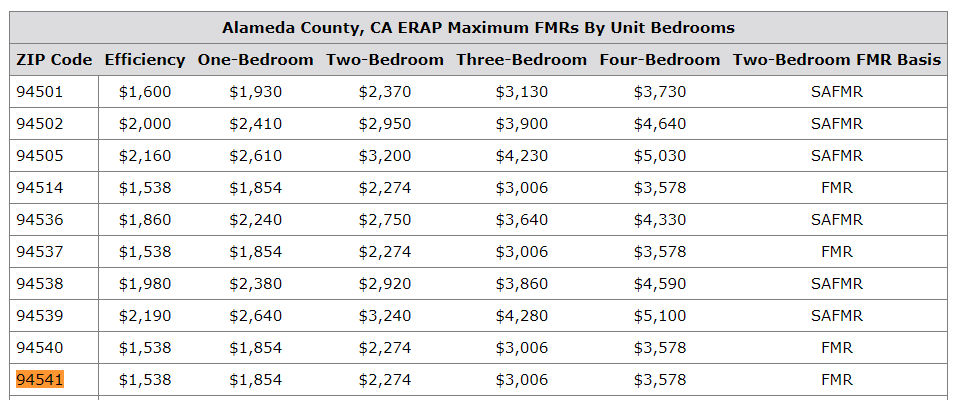

For my 3-bedroom rental in Hayward, California (Alameda County) / zip code 94541), the FMR is $3006 per month.

Add bedrooms

As you can see in the FMR charts above, homes with more bedrooms are more valuable as you can charge more rent. Some ways to add bedrooms is by

- adding an addition to the existing property (this is expensive)

- modifying walls in an existing property to make an extra bedroom (this is relatively cheap)

Let’s say you have a 1200+ sq ft house but it only has 2 bedrooms. Normally, you can easily fit 3 bedrooms in a 1200 sq ft house. The minimum area for a bedroom should be 120 sq ft. The average bedroom size is 132 sq ft. If you happen to have a super large bedroom, e.g. 250 sq ft, you can add a wall in between and turn a huge bedroom into two bedrooms.

Research

When deciding where to invest in a rental property, you often want to look at many factors such as population growth, income growth, appreciation of housing prices, and crime rates. You can find this information from City-Data.

For job growth, you can visit the Department of Numbers. For example, here’s the job growth data for Stockton, CA.

Site-built homes vs manufactured homes

Site-built homes are homes built on site. Most houses are site built. Manufactured homes are built in a factory and assembled on site. Manufactured homes are cheaper than site-built homes with excluding the cost of land. According to this article, the average cost per square foot for a manufactured home is $52 vs $115 for a site-built home. That a big difference.

If you buy a manufactured home and lease the land it’s on, you won’t be able to get a conventional loan / mortgage. Rather, you’d get a chattel loan which is like a loan for personal property (e.g. boat, airplane, etc) since the manufactured home is like personal property. If you buy a manufactured home and the land it is on, you can get a traditional loan / mortgage which offers better rates.

Depending on the cost of land, if might be cheaper to buy land and then buy a bunch of manufactured homes to put on it and then rent them all out rather than build a bunch of homes or a multi-family building on site.

AirBnB (short term) vs traditional (long term) renting

When you rent out your property, you have two options

- long term (traditional)

- short term (e.g. AirBnB)

Though long term rentals provide consistent long term cash flow, you can usually more more money from short term rentals, especially if you have a desirable property in a heavy tourist spot. For example, if you have a 3 bedroom home in downtown San Francisco (94103 zip code), the fair market rent is $4,120 per month. But, if you rent it out on a daily basis via AirBnB for $250 per night, you could get $250 x 30 = $7500 for one month. Of course, there are many other factors so you would need to consider all costs and expenses as well.